The regime of crypto tax in India has drastically changed since the Union Budget 2022. That’s when the Indian government rolled out two rules that every trader now has to live with: a 30% flat tax on gains and a 1% TDS on transactions. Since then, there has been only more confusion and uncertainty, especially as the government is tightening its compliance framework.

In this article, we cut through the noise and guide you through everything you need to know about crypto tax in India , from the basics to the latest updates and exactly how you can generate and file your crypto tax report without a headache.

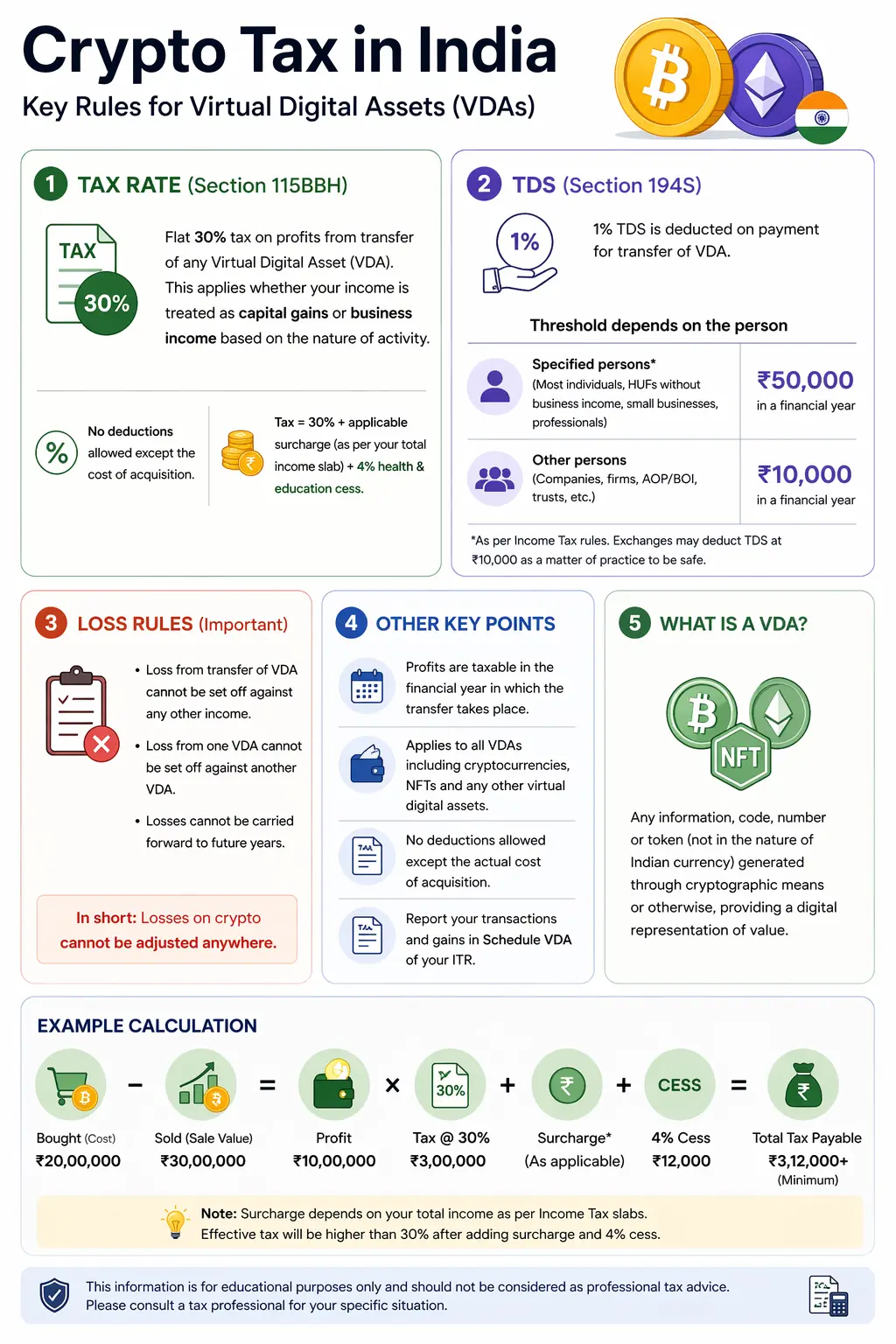

What is the 30% crypto tax in India?

As stated under Section 115BBH of the Income Tax Act, the income that you earn from the transfer of any Virtual Digital Asset (VDA) , including cryptocurrencies, NFTs, and any other digital asset notified by the government , is taxed at a flat rate of 30%. However, this has nothing to do with your income slab. Whether you earn ₹3 lakh/year or ₹3 crore in salary, the rate is the same on your VDA gains. And even if you fall into the non-taxable bracket, any income that you earn from crypto is taxed in the same way.

For high-income taxpayers, a surcharge may apply as well, raising the effective burden even further. Equally important is the no-set-off rule: any loss incurred from a VDA transaction cannot be used to offset gains from another VDA, nor can it be adjusted against any other source of income. Losses also cannot be carried forward to the next financial year, a provision that makes crypto tax in India one of the strictest taxation frameworks in the world.

How does the 1% TDS on crypto work in India?

TDS, which stands for Tax Deducted at Source, comes under Section 194S of the Income Tax Act. The exchange deducts 1% of the value of your crypto sell or trade and deposits it with the Income Tax Department on your behalf. This is not an additional tax on top of the 30% . It is an advance payment towards your final tax liability, which will be due at the end of the year. When you file your ITR at year-end, the TDS deducted will be offset against it. If the amount of TDS deducted is more than what you owe, then you will receive a refund.

The threshold for deduction of TDS is ₹10,000 in a financial year for most, and ₹50,000 for specified people (whose business turnover is under ₹ 1 crore or professional income is under ₹ 50 lakh). Once your transactions on a given exchange cross this threshold within a financial year, the TDS will be applicable to all subsequent transactions via that exchange. This is also an important channel for the Income Tax Department to track crypto activities, as exchanges have to furnish this information to the ITD.

Is there any way to avoid the 30% crypto tax and 1% TDS?

This is a question that has quietly prompted a massive change in the way Indian traders conduct their business, and the answer isn’t so simple. Crypto futures trading has emerged as a potential workaround, and here is why.

When you trade crypto in the spot market, you are buying and selling a virtual digital asset, and so both Section 115BBH (30% flat tax) and Section 194S (1% TDS) are applicable. However, when you trade crypto futures or perpetual contracts, you are not buying or selling the underlying asset. You are simply speculating on the price movement of the underlying market asset using a derivative contract that makes no transfer of the underlying virtual digital asset.

Since no VDA ever changes hands, most tax professionals assert that Section 115BBH does not apply, and Section 194S, which also applies only to VDA transfers, is not applicable either. Consequently, many tax professionals currently treat crypto futures and perpetual contracts as business income taxable at slab rates, since no underlying VDA is transferred. However, this position has not yet been explicitly confirmed by the CBDT, and taxpayers should seek professional advice before adopting this treatment.

This distinction has gained acceptance among many tax practitioners. But we need to understand that this is not a black and white exemption. The Income Tax Department has not issued an explicit clarification on crypto derivatives. Yet tax experts are still split over it, and some argue that a broader reading on the VDA definition may still bring futures under the 30% regime. Filing through ITR-3 under speculative or non-speculative business income is the normal course of action for futures traders at the moment, but it is highly advisable to consult with a qualified chartered accountant before doing so.

What are the latest developments in India’s crypto tax regime?

The regime of crypto tax in India has been becoming progressively stricter and in FY 2025–26 the authorities are looking at a much heightened emphasis on compliance.

The Income Tax Act 2025 has started mandating that crypto exchanges and certain other designated entities have to report crypto-asset transaction data to the Income Tax Department. The move starts from FY 2025-26, and in a bid to bring down the shadow economy, transaction data will be made part of a comprehensive data trail from exchanges to buyers, which will make it difficult for people to under-report crypto transactions.

The new Income Tax Act 2025 has also widened the definition of VDA to include “crypto-assets” (although it does not say exactly what it means by this) and a new penalty framework has been introduced: ₹200 per day for non-reporting and ₹50,000 for inaccurate reporting. India also plans to adopt the OECD’s Crypto-Asset Reporting Framework (CARF) by April 2027, which will require automatic exchange of cross-border crypto transaction data between countries. The efforts to curb money laundering have already registered strong results, with 97 (crypto) asset platforms already registered under PMLA as of December 2024.

Which ITR Form should you file for crypto tax in India?

Crypto gains are reported under Schedule VDA in your Income Tax Return, a dedicated section introduced from AY 2023–24 onward. Here’s which ITR form you should file, depending on how you classify your crypto gains.

- ITR-2: This is the tax form for individual investors who treat their crypto gains as capital gains and do not have business or professional income from any other sources.

- ITR-3: This form is basically for traders who classify crypto; including futures as business income or speculative income.

- Under Schedule VDA, every single transaction must be disclosed with details such as: the name of the coin, the date of acquisition, the date of transfer, cost of acquisition and sale consideration.

- Aggregated or summary-level reporting is not permitted; the ITD requires transaction-by-transaction disclosure.

- Staking rewards and mining income are generally taxed at your applicable slab rate on receipt, with the 30% flat tax applying if you later sell those coins at a profit.

- The ITR filing deadline for non-audit cases in FY 2024–25 was July 31, 2025, with a belated return option available until December 31, 2025.

What if you fail to file your crypto tax in India?

Non-compliance is no longer a grey area. The Income Tax Department is actively using KYC data from domestic exchanges, TDS deduction records, Form 26AS and the Annual Information Statement (AIS) to cross-verify crypto holdings. Non-disclosure of VDA gains may result in a penalty under Sec 270A on the grounds of under-reporting of income (50% of tax payable) or misreporting (200% of tax payable).

Also, the IT Act 2025 has tightened the penalties for non-reporting by exchanges , and by proxy from individual taxpayers , thereby, increasing the risk of getting a tax demand notice for undisclosed crypto income. This risk is likely to increase in the coming years, especially with India’s planned adoption of CARF, which will soon bring cross-border transactions into the government’s line of sight as well.

Why is SunCrypto the perfect platform to generate your crypto tax report?

When filing for crypto tax in India, you need transaction-level data , and for that, you need to source the data from your exchange. And SunCrypto, the simplest and most secure FIU-registered crypto exchange in India, makes this a lot easier with its integration with KoinX, one of the most trusted crypto tax platforms in the country.

SunCrypto’s user interface is designed with Indian users in mind, and with access to and a large variety of digital assets from INR and USDT trading pairs at some of the lowest fees in the market. More importantly though, for tax purposes, SunCrypto’s KoinX integration offers the convenience of automatic syncing of your complete transaction history , trades, transfers, and staking activity , eliminating the need to manually reconstruct your transaction history to file your crypto tax in India. And for actively trading users, this means your crypto tax report is built on complete and accurate data, not estimates or incomplete exports.

How to generate and file your crypto tax report using SunCrypto and KoinX?

The procedure to generate your crypto tax report using the KoinX integration of SunCrypto is simple. Here’s how:

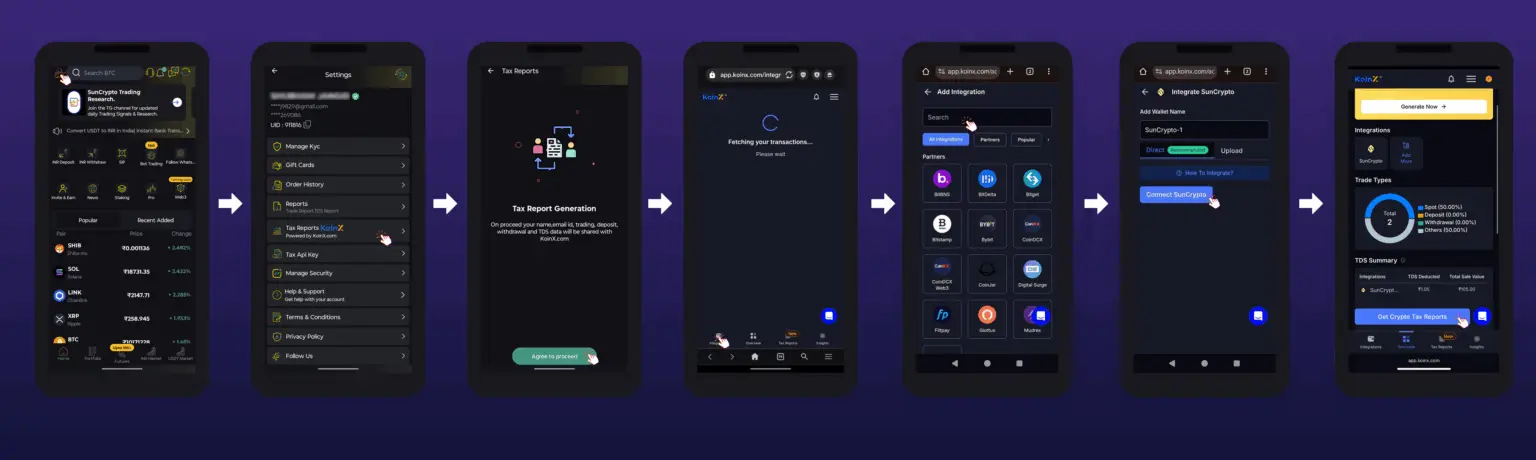

Step1: Connect SunCrypto With KoinX

- Login to your SunCrypto account, navigate to the Profile tab.

- Select Tax Reports KoinX then agree to proceed.

- You will be directed to KoinX where you will click Generate Crypto Tax Report.

- On the left-hand side, click on the Integrations tab.

- From the list, find and select SunCrypto.

- Click Connect SunCrypto. The system will automatically sync your account. A timer of five minutes will show while all of your transactions are imported.

- Alternatively, you can upload your CSV files manually and click submit.

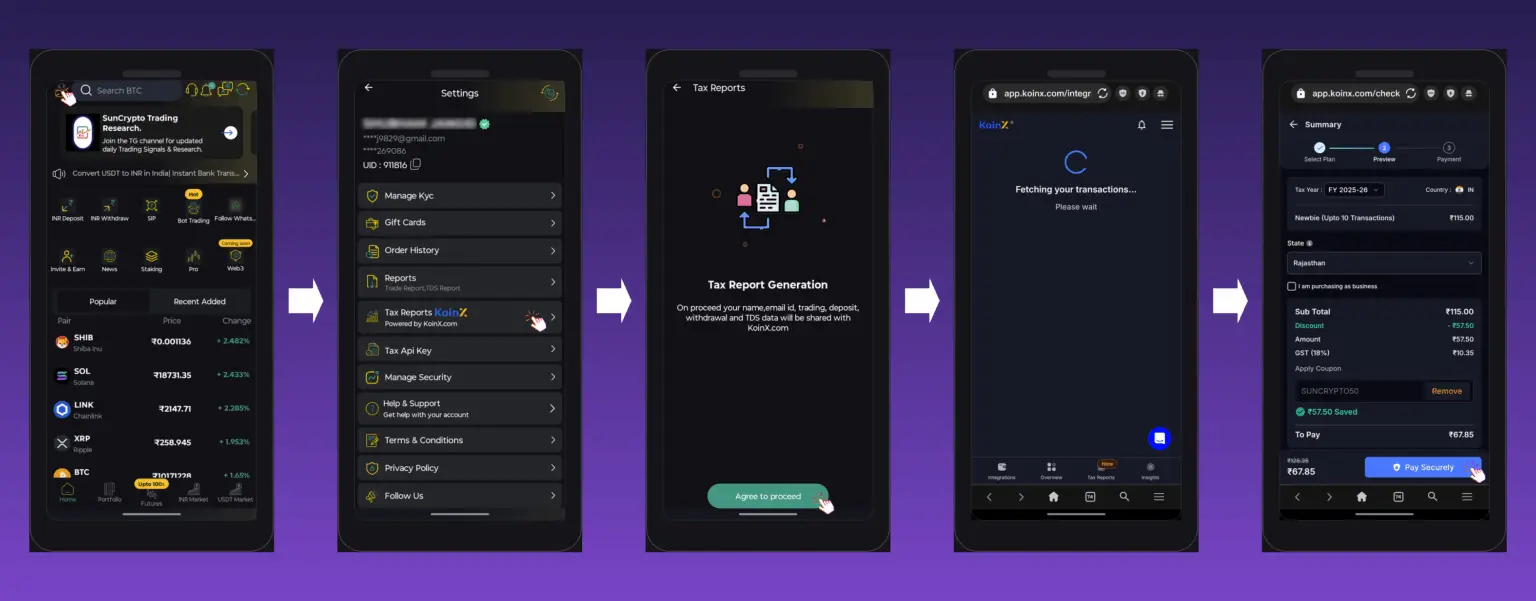

Step2: Review And Confirm

KoinX automatically classifies your transactions by categorizing them as trades, income or transfers. It’s essential to review these where you confirm that your transactions have been categorized correctly before generating your crypto tax report. Because even a single transaction miscategorized can change your final tax liability.

Step3: Generate Your Tax Report

- Login to your SunCrypto account again and follow the same steps – Profile → Tax Reports KoinX → Agree to Proceed.

- From KoinX, select the financial year for which you would like to file your crypto tax.

- KoinX will automatically calculate your tax liability based on your entire transaction history for that year.

- After the calculations are complete, the tax report will be generated for you to use to file your ITR.

Note: You can generate your crypto tax report for free, but to file your tax report, you’ll have to pay a small amount of fee that will depend on your transactions.

Things to Remember

- Always choose a financial year that corresponds to your transaction export dates to prevent having incomplete data in your report.

- Make sure your exports have staking rewards and inter-wallet transfers , not just spot trades.

- Avoid uploading the same CSV more than once, as this will create duplicate entries and produce an inaccurate report.

Final Thoughts

The regime of crypto tax in India is one of the strictest in the world, and it is just getting stricter every year. Knowing the rules for crypto tax in India, the 30% flat rate, the 1% TDS, the no-set-off clauses, and the new mandatory reporting obligations, is no longer optional for any serious trader or investor. Filing correctly and in a timely manner is not only a compliance requirement but also the most financially prudent thing you can do, given the penalties and scrutiny for non-disclosure.

For Indian traders who want to avoid hassle, SunCrypto’s partnership with KoinX combines the precision of exchange-level accuracy with the intelligence of a tax platform to streamline the entire process, from syncing your transaction history to generating a detailed ITR-ready tax report, so you can spend your time and effort on what matters most: Trading smart.

Can I offset a loss in one crypto against a profit in another crypto?

No, under Indian Income Tax law, you cannot offset a loss from one cryptocurrency against a profit in another cryptocurrency.

Can I carry forward crypto losses to next year?

No, you cannot carry forward crypto losses to future financial years in India. Under Section 115BBH of the Income Tax Act, any loss incurred from the transfer of Virtual Digital Assets (VDAs) cannot be carried forward to subsequent assessment years.

Will TDS be deducted if I trade on a foreign crypto exchange?

If you trade on a foreign crypto exchange, the platform itself will not automatically deduct TDS (Tax Deducted at Source) on your behalf. Under Indian tax law, you are legally responsible for self-deducting and depositing the 1% TDS on all eligible cryptocurrency transactions manually.